Weekly Economics Report - April 10 2026

US laboUr market posts largest jobs gain in 15 months, but clouds brewing from Iran war

WASHINGTON, April 3 (Reuters) - U.S. job growth rebounded more than expected in March as a strike by healthcare workers ended and temperatures warmed up, but downside risks for the labor market are mounting from a war with Iran that has no clear end in sight.

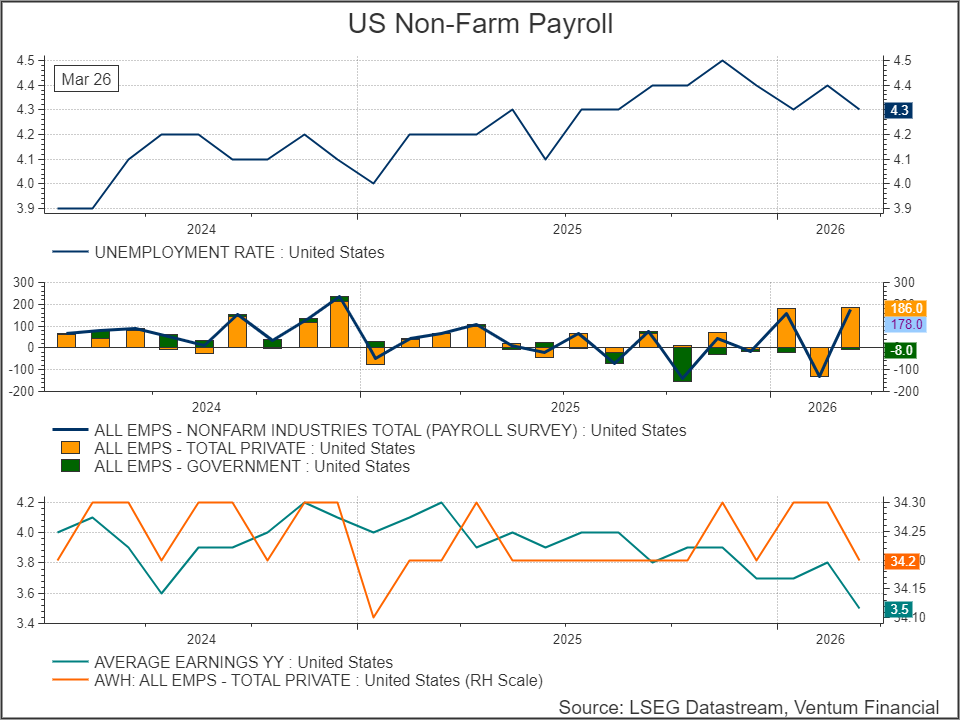

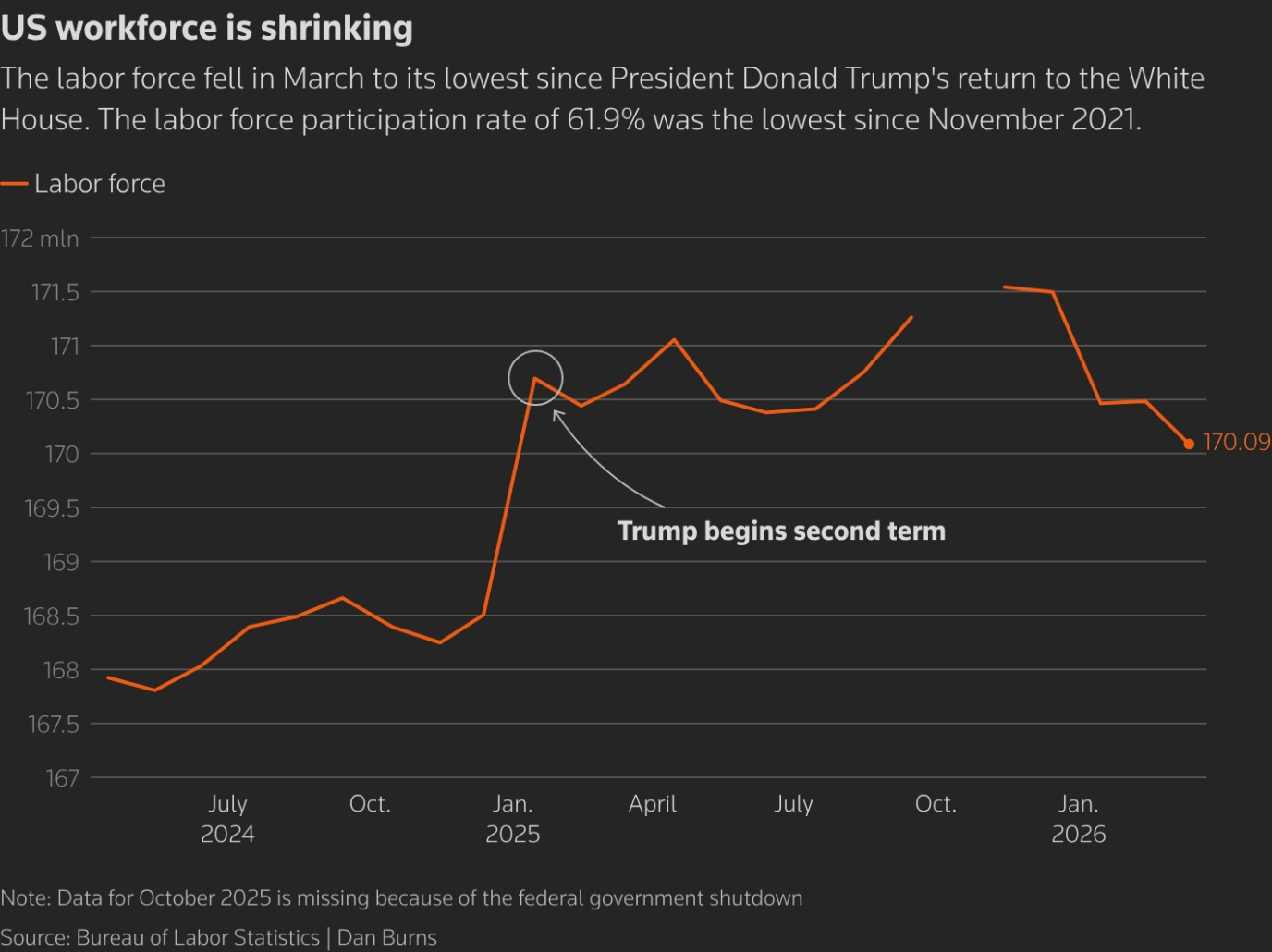

The biggest increase in nonfarm payrolls in 15 months, and also the largest since President Donald Trump returned to the White House, followed a sharp decline in February, the Labor Department's closely watched employment report showed on Friday.

Nonetheless, the rebound exaggerates the labor market's health. The average workweek was shorter last month and annual wage growth increased at its slowest pace in nearly five years.

While the unemployment rate fell to 4.3% from 4.4% in February, that was because 396,000 people dropped out of the labor force, more than offsetting weakness in household employment. The labor force participation rate fell below 62% for the first time since the COVID-19 pandemic.

Economists said March was too early to capture the fallout from the Middle East conflict.

"This is an on-the-one hand, on-the-other kind of a job market," said Bill Adams, chief U.S. economist at Fifth Third Commercial Bank. "This report tells us next to nothing about the Iran war's impact on the job market."

Nonfarm payrolls increased by 178,000 jobs last month, the most since December 2024, after a downwardly revised 133,000 drop in February, the Labor Department's Bureau of Labor Statistics said. Economists polled by Reuters had forecast payrolls rising by 60,000 jobs after a previously reported 92,000 decrease in February.

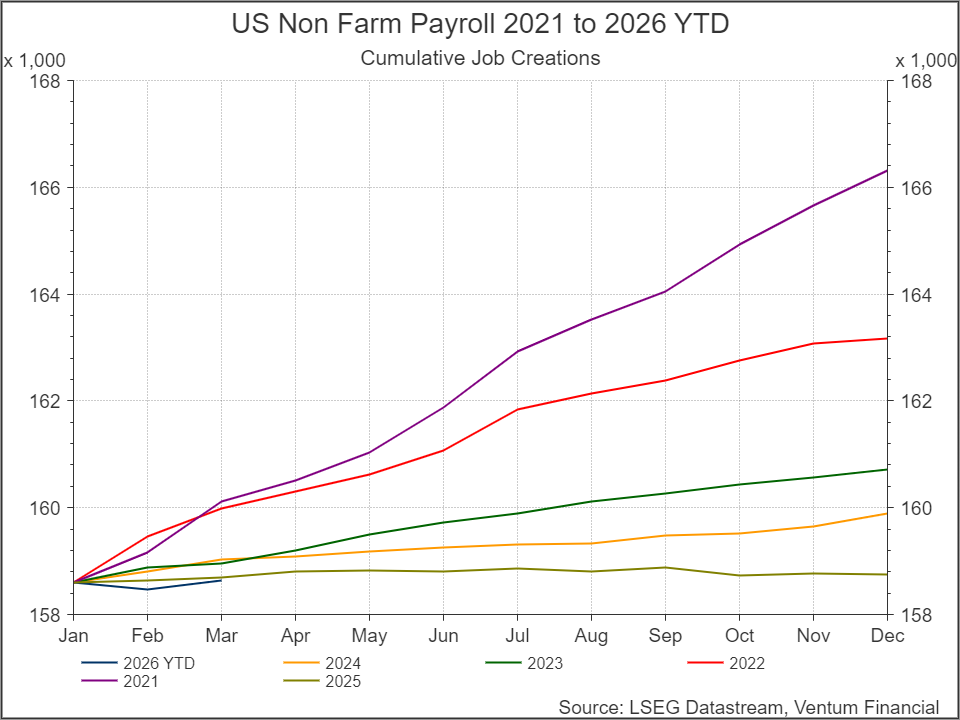

Estimates ranged from a loss of 25,000 positions to a gain of 125,000 jobs. The economy has experienced months of positive and negative payrolls since May last year, with volatility intensifying this year. Economists attributed some of the choppiness to the birth-death model, which the government uses to estimate how many jobs were gained or lost because of companies opening or closing in a given month.

Others blamed uncertainty related to Trump's sweeping import tariffs, which have since been struck down by the U.S. Supreme Court. Trump, however, responded by imposing a global tariff for up to 150 days.

Job growth averaged 68,000 per month in the first quarter, which economists said was a better reflection of the labor market's health. Data from the BLS this week showed job openings decreased by the most in nearly 1-1/2 years in February, pointing to slipping labor demand.

March's employment report likely has no impact on the interest rate outlook, with the effects of supply chain disruptions from the conflict still to work their way through the economy. The odds of a rate cut this year have greatly diminished. The Federal Reserve left its benchmark overnight interest rate in the 3.50% to 3.75% range last month.

U.S. Treasury yields rose on the report. The stock market was closed for the Good Friday holiday.

"Since May 2025, each month of positive job growth has been followed by a month of negative growth, a pattern that likely reflects the tariff uncertainty that began in April," said Olu Sonola, head of U.S. economics at Fitch Ratings. "The war in Iran now threatens to add to that choppiness, especially if the conflict drags on and the uncertainty impulse intensifies. For the Fed, wait-and-see is the only sensible option at this point."

HEALTHCARE DOMINATES JOB GROWTH

The war, now in its second month, has boosted global oil prices by more than 50%. Trump on Wednesday vowed more aggressive strikes on Iran.

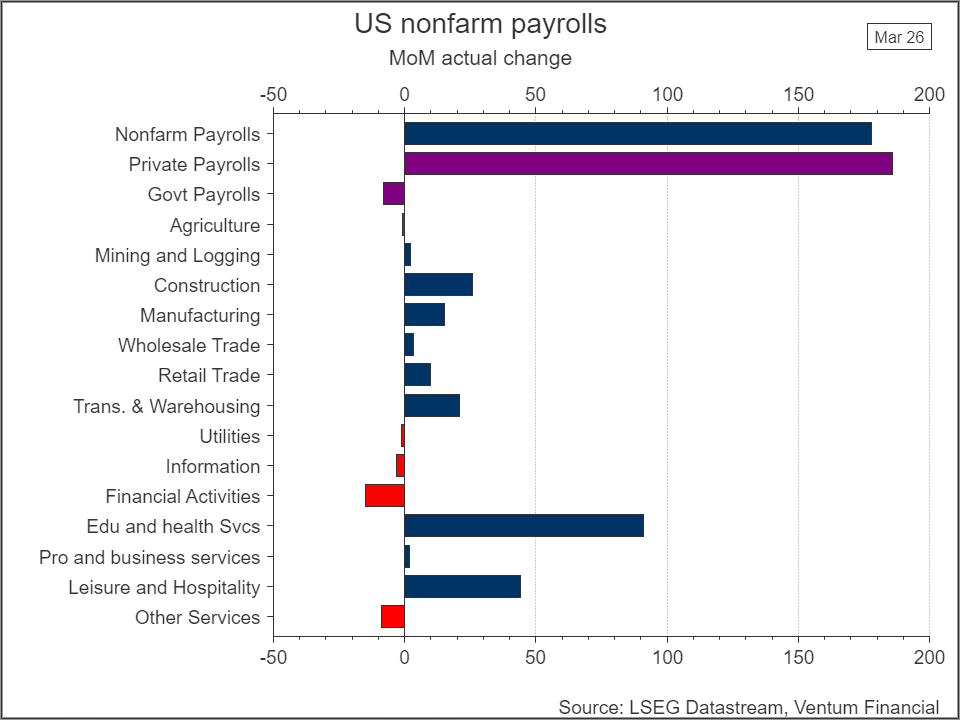

The healthcare sector dominated the nearly broad increase in employment, adding 76,000 positions as 35,000 employees at doctors' offices returned to work following a strike. Employment also increased at hospitals.

Construction employment increased by 26,000 jobs. Transportation and warehousing payrolls advanced by 21,000 positions, though employment in the sector remained down by 139,000 since peaking in February 2025.

There were further gains in social assistance employment. Manufacturing, which the Trump administration is trying to shore up with import duties, saw payrolls increasing by 15,000 jobs - the biggest gain since November 2023. Still factory payrolls are down 82,000 since January 2025.

Leisure and hospitality employment rebounded 44,000, with the bulk of the increase at restaurants and bars. Federal government employment declined by another 18,000 jobs, and is down 355,000, or 11.8% since peaking in October 2024. The White House embarked on an unprecedented campaign to slash the size of federal agencies, which Trump argued were bloated. The federal government is, however, now actively recruiting workers.

The financial activities sector shed more workers. There were signs of the adoption of artificial intelligence leading to job losses in the professional and business services sector, where positions for computer systems design and related services dropped by 13,200.

The share of industries reporting job growth increased to 56.8% from 49.2% in February. But the workweek eased to 34.2 hours from 34.3 hours. A single month does not make a trend, but businesses will first reduce hours before resorting to layoffs.

Average hourly earnings rose 0.2% after increasing 0.4% in February. Wages increased 3.5% year-on-year, the smallest gain since May 2021, after advancing 3.8% in February. With the national average retail gasoline price topping $4 a gallon this week for the first time in more than three years, households' purchasing power will be squeezed. The war wiped about $3.2 trillion from the stock market in March.

Details of the household survey, from which the unemployment rate is calculated, were mostly weak. The survey response rate, however, dropped to an all-time low of 63.9% from 65.9% in February.

Household employment decreased by 64,000 and more people worked part-time for economic reasons. The labor force participation rate dropped to 61.9%, declining below 62% for the first time in nearly 4-1/2 years in part as immigration flows ebb and the workforce ages.

Economists estimated the jobless rate would have risen to 4.5% were it not for the decline in the participation rate. A reduced labor force now means the economy needs to create fewer than 50,000 jobs per month to keep up with growth in the working-age population.

"The labor force is structurally tighter now than it was before COVID," said Gus Faucher, chief economist at PNC Financial Services. "The decline in the labor force participation rate since the pandemic recovery is coming from an aging workforce, and more recently the crackdown on immigration."

US service sector cools in March; price paid measure highest in 3-1/2 years

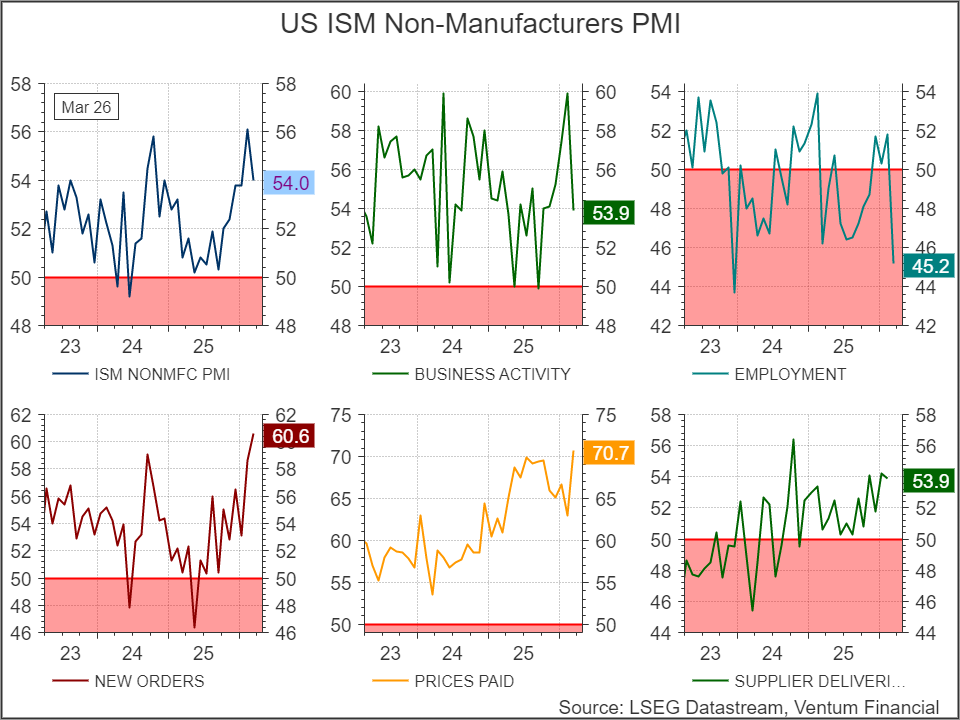

WASHINGTON, April 6 (Reuters) - U.S. services sector growth slowed in March, while prices paid by businesses for inputs climbed to near a 3-1/2-year high, an early sign that the prolonged war with Iran was boosting inflation pressures.

The Institute for Supply Management said on Monday its nonmanufacturing purchasing managers index slipped to 54.0 last month from 56.1 in February. Economists polled by Reuters had forecast the services PMI dipping to 54.9. A reading above 50 indicates growth in the services sector, which accounts for more than two-thirds of U.S. economic activity.

The U.S.-Israel conflict with Iran, now in its second month, has boosted global oil prices by more than 50%. The national average retail gasoline price has jumped above $4 a gallon for the first time in more than three years. Economists expect the inflation hit from the war would show in the March Consumer Price Index report scheduled to be released on Friday.

Producer prices already increased in February in anticipation of the escalation in the Middle East conflict.

The ISM survey's measure of prices paid by businesses for inputs soared to 70.7, the highest reading since October 2022, from 63.0 in February.

This gauge had remained elevated, with businesses blaming rising costs from President Donald Trump's broad tariffs, which have since been struck down by the U.S. Supreme Court. But Trump responded by imposing a global tariff for up to 150 days.

The survey's measure of supplier deliveries increased to 56.2 from 53.9 in February. A reading above 50 percent indicates slower deliveries. That mirrored a lengthening in delivery times at factories, with manufacturers of food, beverages and tobacco products citing "container delays."

The anticipated inflation fallout from the conflict has greatly diminished the odds of an interest rate cut this year. The Federal Reserve left its benchmark overnight interest rate in the 3.50% to 3.75% range last month.

The survey's measure of new orders increased to a two-year high of 60.6 from 58.6 in February. But export order growth slowed considerably and the increase in unfinished work moderated.

Services sector employment contracted, with the jobs measure dropping to the lowest level since December 2023. That is at odds with a sharp rebound in job growth in March, which was driven by a 143,000 increase in private service-providing payrolls. The ISM employment gauge has, however, not been a good predictor of private services payrolls in the Labor Department's employment report.

China services activity growth cools in March, private PMI shows

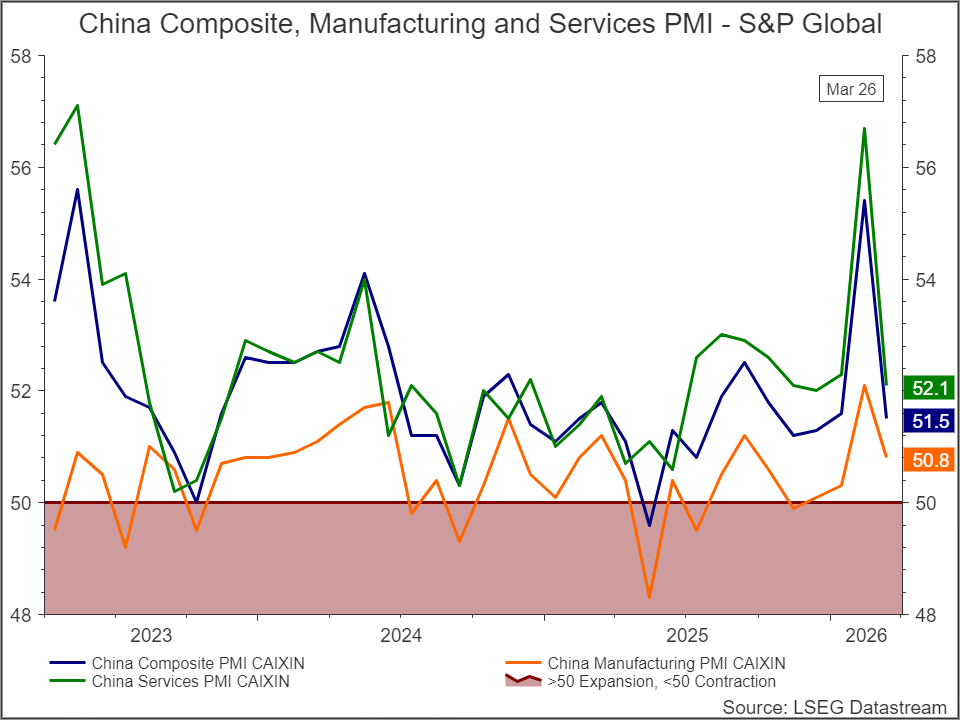

BEIJING, April 3 (Reuters) - Growth in China's services activity slowed in March from February's 33-month high, as softer demand and a decline in overseas orders weighed on momentum, a private-sector survey showed on Friday.

The RatingDog China General Services purchasing managers' index, compiled by S&P Global, fell to 52.1 in March from 56.7 in February, remaining above the 50-point mark that separates expansion from contraction.

The reading contrasted with an official survey released earlier this week showing services activity edged up in March, partly because the two surveys cover different samples.

China's economy started the year on a firmer footing with a surge in exports driven by AI-related technology demand, quickening industrial output, and a rebound in retail sales and investment.

But escalating conflict in the Middle East has rattled global trade and energy markets, clouding the outlook for the world's second-largest economy.

China remains relatively well-positioned to endure short-term disruptions from the Iran conflict, said Lynn Song, chief economist of Greater China at ING, in a research note this week, adding "but if higher energy prices and shipping disruptions persist or worsen, we could see pressure build in the months ahead."

New business expanded at the slowest pace since April 2025, while new export orders contracted in March after rising the previous month.

Services firms cut staffing at the fastest pace in six months, citing resignations, retirements, unfilled vacancies and restructuring.

Average input costs in the services sector continued to rise in March, with the sub-index at 50.7 versus 50.9 in February, driven by higher fuel, raw materials and labour costs.

The modest increase in cost pressures allowed service providers to lower prices to help support sales.

Business sentiment for the year ahead remained positive, though it eased slightly from February, the survey showed.

The composite output index, which includes both manufacturing and services activity, fell to 51.5 in March from 55.4 in February.

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies .Ventum Financial Corp.

www.ventumfinancial.com

Ventum Financial Corp. www.ventumfinancial.com

Vancouver Office

2500 - 733 Seymour Street

Vancouver, BC V6B 0S6

Ph: 604-664-2900 | Fax: 604-664-2666

For a complete list of branch offices and contact information, please visit our website.

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre - Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited.

For further disclosure information, reader is referred to the disclosure section of our website.

Share this post