Weekly Economics Report - March 9 2026

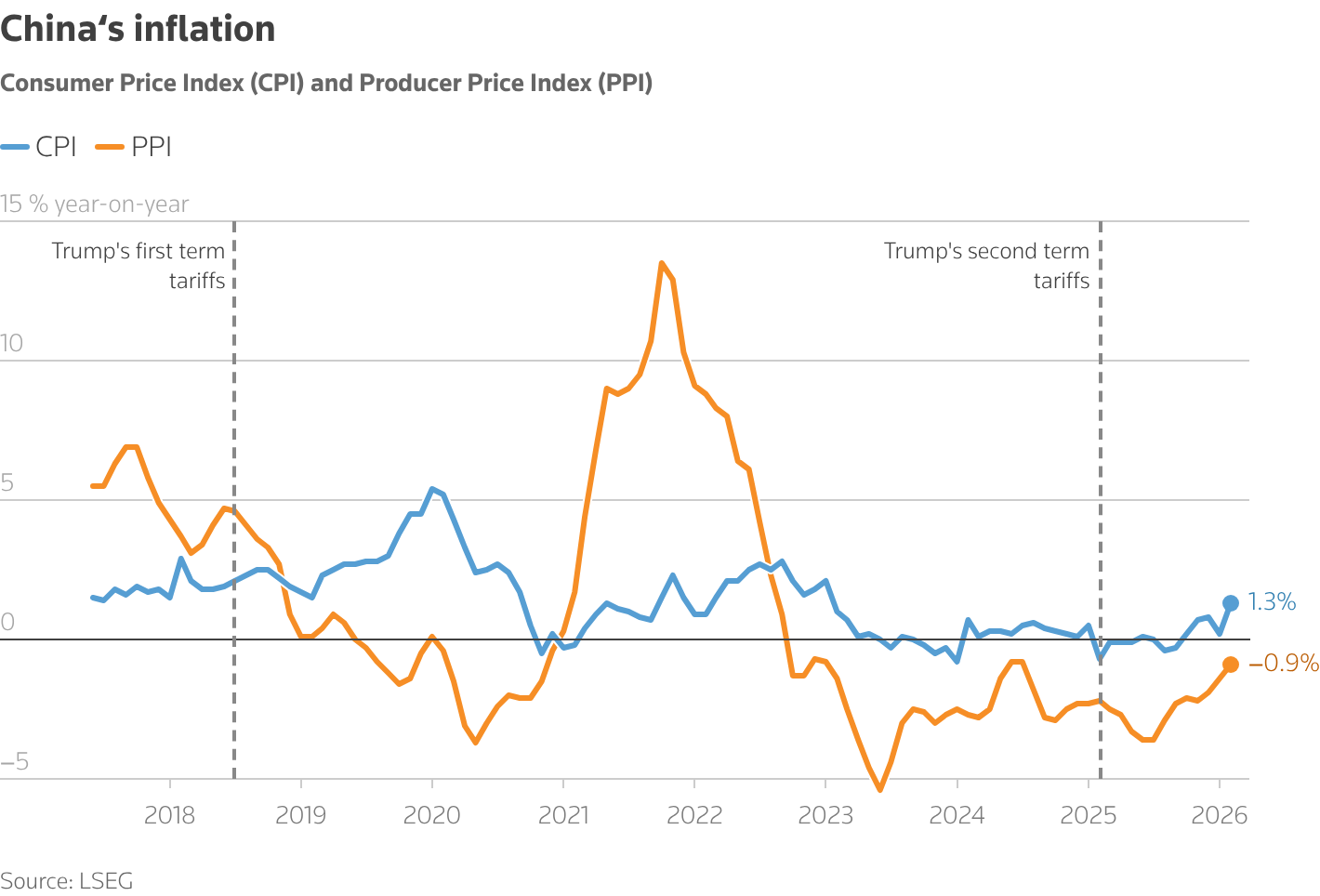

China consumer inflation hits 3-yr high on holiday surge, producer deflation lingers

BEIJING, March 9 (Reuters) - China's consumer inflation accelerated to the highest in more than three years due to the effects of the Lunar New Year holiday, while producer deflation persisted as weak demand remained a drag on an economy facing stiff external challenges.

Policymakers have been trying to boost consumption over the past two years, but analysts say more needs to be done to address the supply-demand imbalance.

The consumer price index (CPI) rose 1.3% year-on-year for the fifth month of gains and outpaced the 0.2% increase in January, data from the National Bureau of Statistics (NBS) showed on Monday. The rate was the highest in 37 months, and beat an expected 0.8% rise in a Reuters poll.

A nine-day Lunar New Year holiday boosted domestic travel and consumer spending, lifting the headline CPI as services prices surged. Flight ticket prices rose 29.1% year-on-year, while gold jewellery prices soared 76.6%, according to NBS data. Analysts said it was uncertain whether the recovery in consumer prices could last.

"Tensions in the Middle East will push inflation higher for as long as global energy prices remain elevated," said Zichun Huang, China economist at Capital

Economics, referring to a rapid jump in oil prices in the wake of the U.S. and Israeli strikes against Iran.

However, China's five-year plan unveiled at a key parliament meeting last week disappointed "in terms of boosting domestic demand," Huang said, meaning "any inflationary pickup will unwind once tensions ease."

Core CPI, which excludes volatile prices of food and fuel, rose 1.8% year-on-year, compared with the 0.8% uptick in January. On a monthly basis, CPI increased 1% versus a 0.2% rise in January and an expected 0.5% gain.

CiOIL SHOCK REARS HEAD AS DEFLATION PERSISTS

The economy has been beset by a years-long property market slump and external trade uncertainties, with protectionist U.S. policies posing fresh challenges to policymakers.

Beijing has vowed to keep cracking down on excessive competition and ensure smoother exit of inefficient production capacity in order to stabilise prices.

However, the deflationary impulse across the economy continues to exert margin pressure on the manufacturing sector, while underpinning expectations of sustained price falls in a further blow to confidence.

There was a modicum of relief in the latest data, however. The producer price index (PPI) recorded the smallest year-on-year drop since July 2024, having fallen 0.9% in February. It declined 1.4% the previous month, and the Reuters poll had forecast a 1.2% drop.

In a statement, NBS statistician Dong Lijuan attributed the milder producer deflation to factors including stronger prices in advanced and emerging sectors as well as capacity management in key industrial sectors.

PPI rose 0.4% in February from January, driven partly by rising crude oil prices globally and demand linked to growth in computing power, Dong said.

Beijing is aiming for GDP growth of between 4.5% and 5% for the year, slower than the previous year's "around 5%", signalling willingness to accommodate reforms that could help the economy reduce its reliance on external demand.

The government's CPI target for 2026 remained unchanged at "around 2%", a goal that China's state planner said was "conducive to guiding public expectations and boosting market confidence while also leaving room for macro regulation and further reforms".

China has not achieved its annual CPI goals for years.

The government has pledged to implement "more proactive" macroeconomic policies in 2026. The central bank in January cut sector-specific interest rates and earmarked more cheap loans to small and medium-sized tech and private firms.

"Unless the oil price shock is notably stronger and longer than expected, it's not expected that inflation will inhibit PBOC easing this year," Lynn Song, chief economist for Greater China at ING, said.

There is room for a rate cut in the second quarter as the economy likely got off to a soft start in 2026, Song added, though policymakers can choose a more cautious route and delay the easing.

Middle East conflict sticks 2026 consensus trades into reverse

March 9 (Reuters) - The escalating war in the Middle East has investors questioning some of 2026's most popular trades and themes, with global equities slumping, the dollar jumping and traders scaling back their bets for rate cuts from the Federal Reserve.

"This year, investors have been positioning for growth. A stagflationary shock was not part of the plan," said ING head of global markets Chris Turner.

"Investors are looking at things cautiously and would still have more to unwind."

Here are five popular themes that have been upended by the conflict in the Middle East:

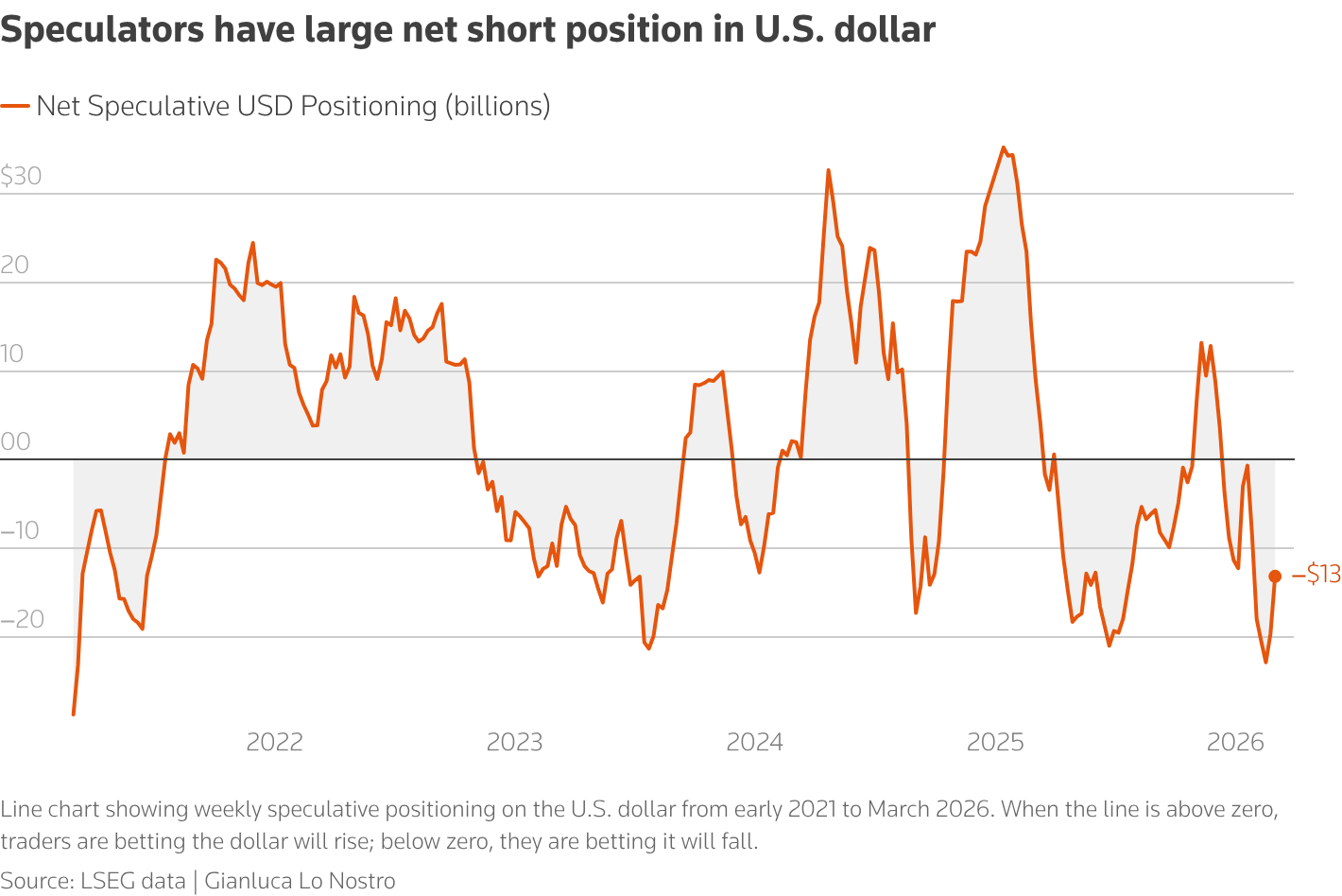

1/ DOLLAR SHORTS SQUEEZED

Investors had been holding their largest bearish bet on the dollar since 2021 as recently as last month, according to weekly data from the U.S. markets regulator.

Expected rate cuts from the U.S. Federal Reserve gave little incentive to buy too heavily into the U.S. currency. But after the start of the conflict, the dollar has hit its strongest level since last November, in a sign of a rush to safety. "The U.S. dollar emerges as the biggest winner of the Middle East conflict," said Ipek Ozkardeskaya, senior analyst at Swissquote. "The U.S. economy will likely be more resilient to energy shocks."

The U.S. is a net energy exporter these days and imports just 17% of its needs, a 40-year low, according to Jean-François Robin, head of global research at Natixis CIB.

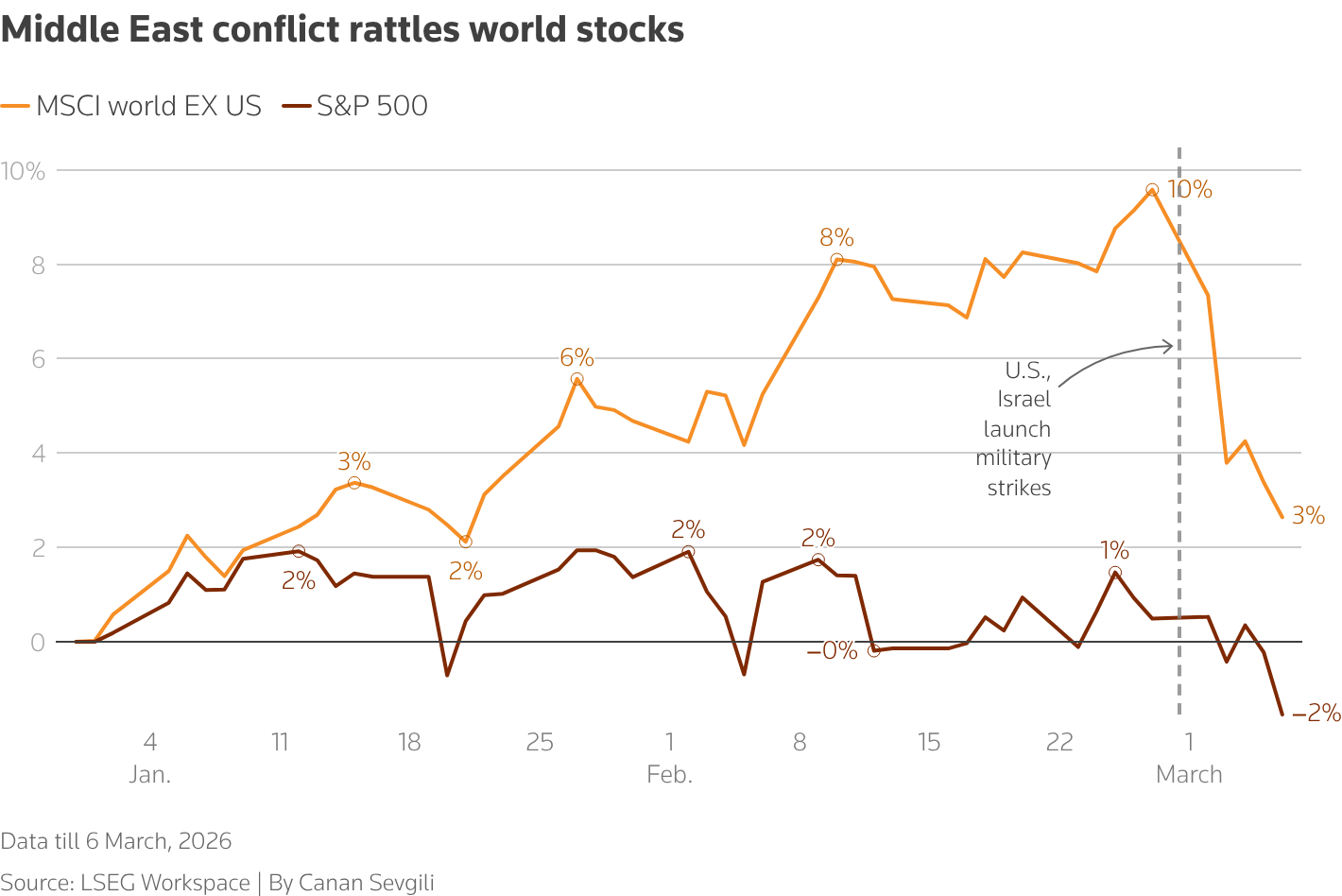

2/ REST OF WORLD EQUITIES SLUMP

Global equities, which began 2026 supported by a broad "buy equities" consensus, have slid sharply.

The MSCI World ex‑US index .MIWU00000PUS fell abruptly after the U.S. and Israeli strikes on Iran, while the S&P 500 .SPX proved more resilient as investors favoured the U.S., given the economy is less reliant on energy imports.

"The conflict hasn't destroyed the 2026 long-equities thesis, but it has made it far more rate- and oil-dependent," said Lale Akoner, global market strategist at eToro, adding that if energy keeps inflation sticky, "multiples, not earnings, are the weak link."

She said earlier signs of leadership broadening beyond the United States have faded as investors returned to the depth and liquidity of U.S. markets. Swissquote's Ozkardeskaya said the shock could shift flows toward energy-rich markets and weigh on energy-dependent economies, potentially halting the rotation from the U.S. to Europe and Asia.

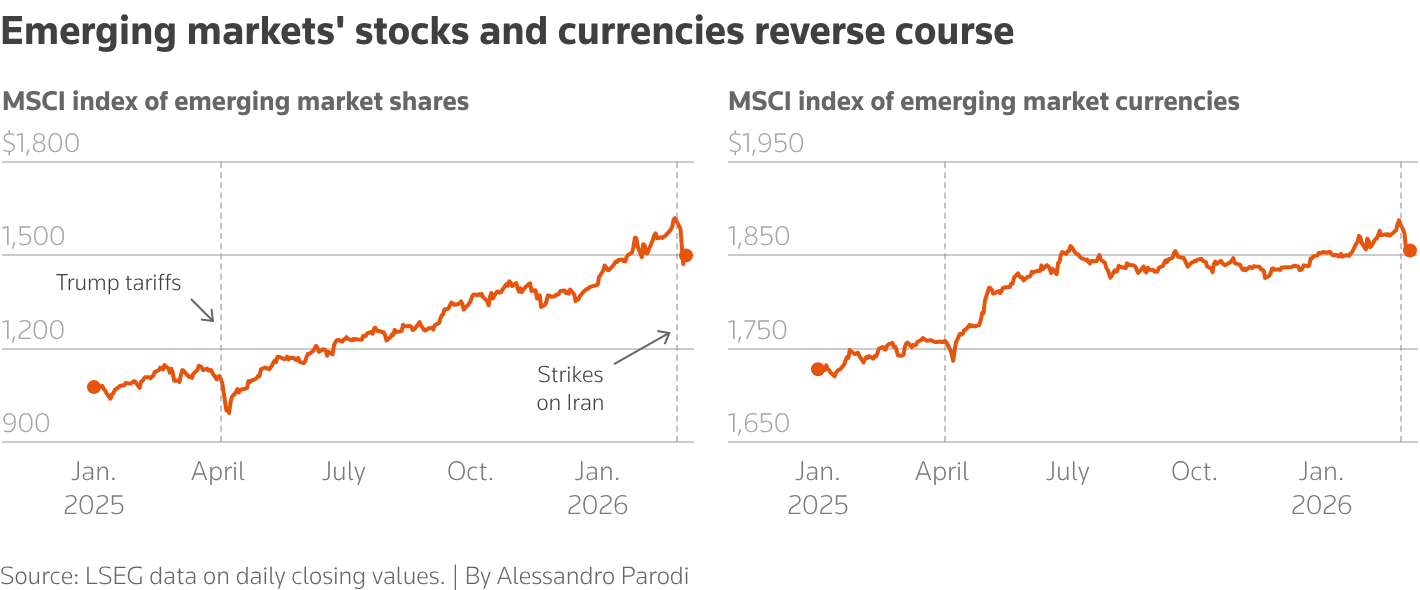

3/ EMERGING MARKETS RATTLED

Emerging markets stocks and currencies were strong performers at the beginning of the year, with a jump of over 15% in EM stocks .MIEF00000PUS and a 1.9% rise in MSCI's index of emerging market currencies .MIEM00000CUS until last Friday.

But the two indexes lost 7% and 1.5% respectively last week, with sharp falls in strong year-to-date performers such as South Korea's Kospi .KS11.

"The biggest underperformers this week were the outperformers between January and February," Goldman Sachs said about emerging currencies in a note to clients on Wednesday.

The brokerage said de-risking was strongest in markets most exposed to the Middle East and oil shocks, such as Egypt, the United Arab Emirates and Thailand, and last year's outperformers like Korea, Brazil and South Africa.

Analysts at JPMorgan moved EMEA emerging market FX to 'marketweight' on Tuesday, and added Poland's zloty to their list of 'underweight' currencies, saying central and eastern Europe is particularly exposed to energy prices.

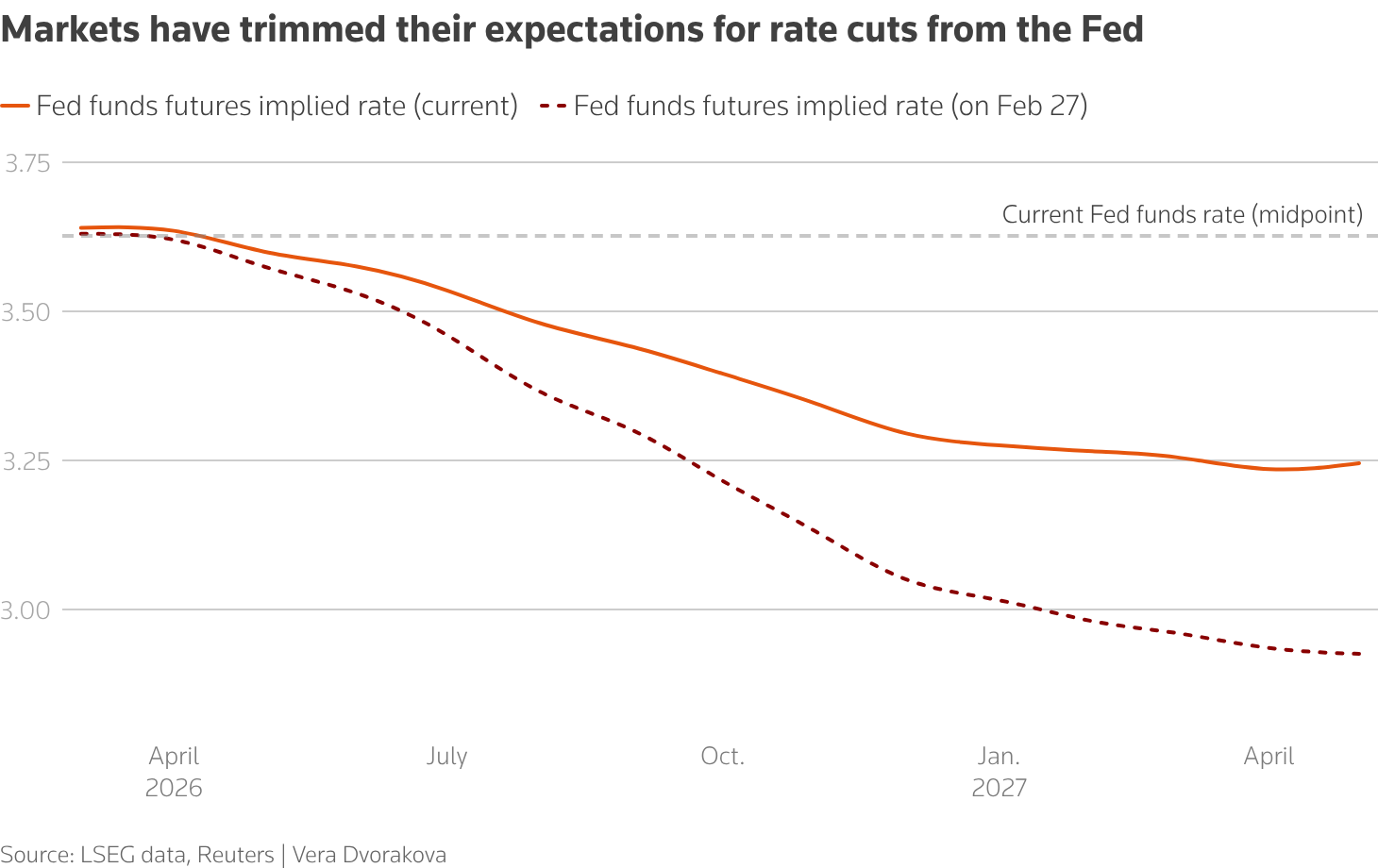

4/ FED RATE CUTS IN DOUBT

Surging energy prices stoked inflation worries and pushed traders to moderate their expectations on interest-rate cuts by the Fed. Prior to the start of the conflict, markets had expected around a 50% chance of a rate cut at the June meeting, which would be the first under its new chairman. That has now been cut to around 25%.

The recent energy shock has pushed markets to scale back expectations for interest-rate cuts for the Bank of England and traders are now pricing for the European Central Bank to raise rates, rather than cut, this year. "Some of the largest shifts in 2026 G10 central bank pricing have come in economies which were priced for further easing this year," Goldman Sachs said.

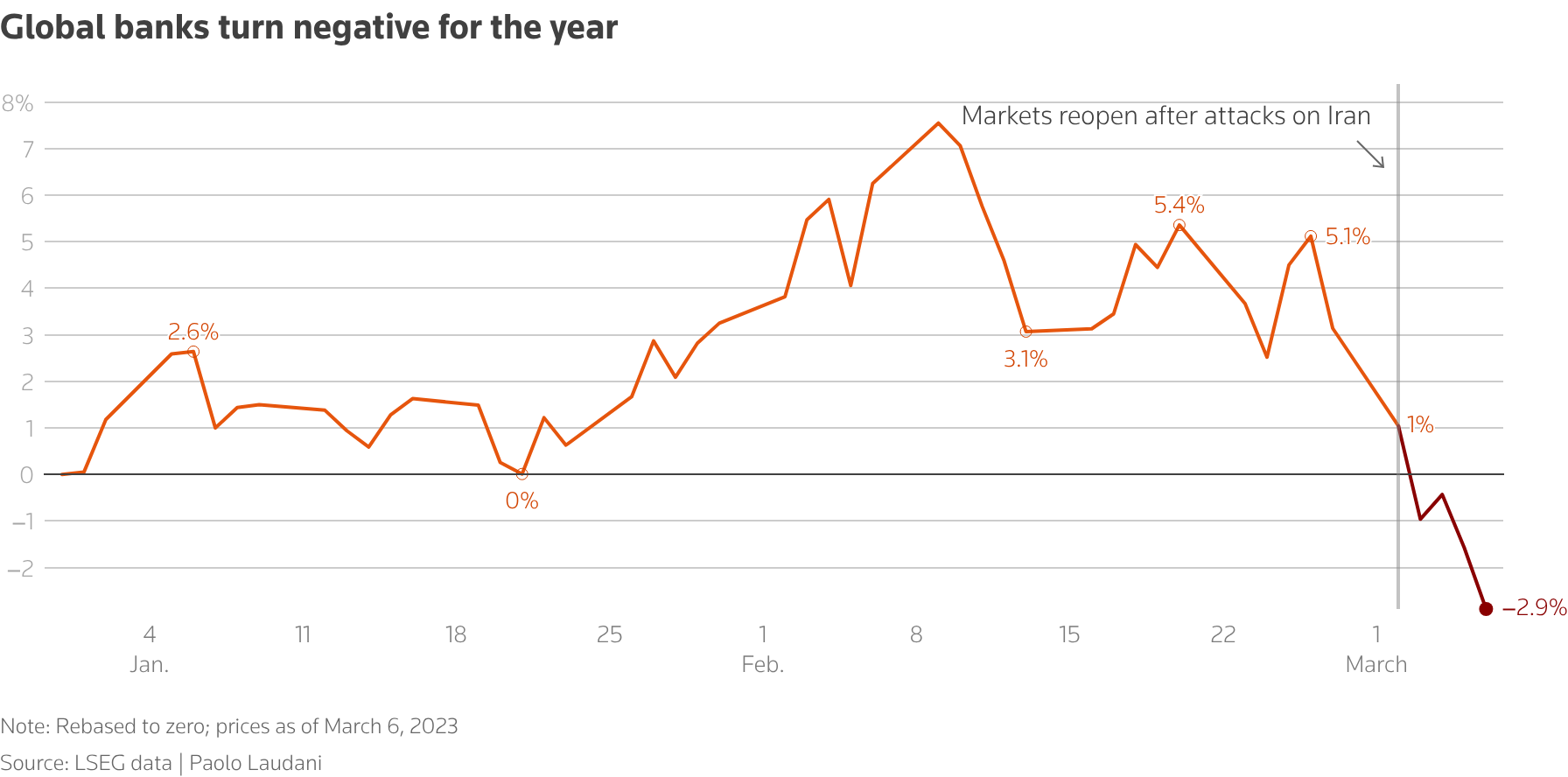

5/ BANKS

Banking stocks .MIWO0BK00PUS — which had logged modest gains earlier in 2026 — have fallen as investors reassess the economic fallout from disruption in the Strait of Hormuz.

The risk of higher energy costs fed fears that broader inflation pressures could return, raising the prospect of slower lending and weaker credit demand even if rates remain elevated.

While higher interest rates typically support bank margins, renewed inflation worries can curb borrowing and investment.

"The key risk to watch is credit spreads and private-market liquidity; geopolitical headlines matter mainly if they translate into tighter financial conditions," eToro's Akoner said.

© 2018-2023 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. Refinitiv and the Refinitiv logo are trademarks of Refinitiv and its affiliated companies .Ventum Financial Corp.

www.ventumfinancial.com

Ventum Financial Corp. www.ventumfinancial.com

Vancouver Office

2500 - 733 Seymour Street

Vancouver, BC V6B 0S6

Ph: 604-664-2900 | Fax: 604-664-2666

For a complete list of branch offices and contact information, please visit our website.

Participants of all Canadian Marketplaces. Members: Canadian Investment Regulatory Organization, Canadian Investor Protection Fund and AdvantageBC International Business Centre - Vancouver. Estimates and projections contained herein are our own and are based on assumptions which. we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness, nor in providing it does Ventum Financial Corp. assume any responsibility or liability. This information is given as of the date appearing on this report, and Ventum Financial Corp. assumes no obligation to update the information or advise on further developments relating to securities. Ventum Financial Corp. and its affiliates, as well as their respective partners, directors, shareholders, and employees may have a position in the securities mentioned herein and may make purchases and/or sales from time to time. Ventum Financial Corp. may act, or may have acted in the past, as a financial advisor, fiscal agent or underwriter for certain of the companies mentioned herein and may receive, or may have received, a remuneration for their services from those companies. This report is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities and is intended for distribution only in those jurisdictions where Ventum Financial Corp. is registered as an advisor or a dealer in securities. Any distribution or dissemination of this report in any other jurisdiction is strictly prohibited.

For further disclosure information, reader is referred to the disclosure section of our website.

Share this post